Want more content?

By subscribing to our mailing list, you will be enrolled to receive our latest blogs, product updates, industry news, and more!

Want more content?

By subscribing to our mailing list, you will be enrolled to receive our latest blogs, product updates, industry news, and more!

What is network tokenization?

Network tokenization is a type of payment card tokenization offered by the payments network—Visa, Mastercard, Discover, American Express, etc.—that replaces primary account numbers (PANs) and other card details with a token issued by the card brand.

When implemented properly, network tokenization ensures secure remote commerce throughout the payments ecosystem by removing the need for merchants or third-party providers to expose themselves to the risk of handling the raw PAN and other sensitive cardholder data.

How Network Tokenization Works

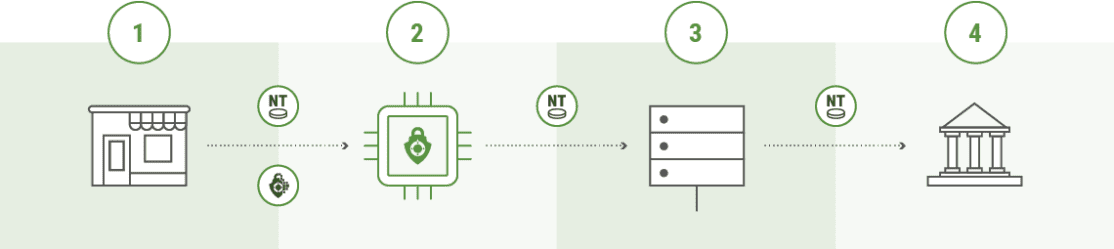

- The client sends TokenEx a PAN or TokenEx token in a request for a network token.

- TokenEx generates the request for a network token and passes it to the card network.

- The card network sends the network token request to the card issuer.

- The card issuer provisions the network token, which is then returned to the client via TokenEx.

Similar to standard provider tokenization, network tokenization works by exchanging sensitive cardholder data, such as the PAN, for a nonsensitive placeholder called a token that offers the same functionality as the original data without the associated risk.

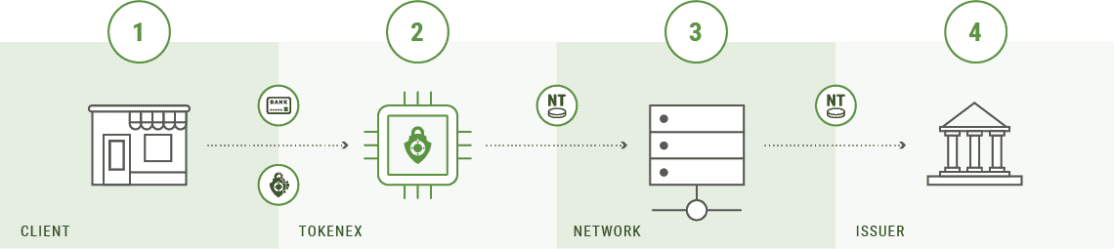

- The client sends a payment authorization to TokenEx with a TokenEx token or a network token.

- TokenEx passes the payment authorization with the network token and cryptogram to the client’s payment gateway.

- The payment gateway passes the payment authorization to the payments network.

- The issuer approves the payment transaction.

The primary difference between other forms of tokenization and network tokenization is that network tokens are issued by the card brands themselves, which means the tokens can be used at each step of the payment process. Unlike network tokens, provider tokens require the merchant or third party to first collect raw cardholder data, and expose themselves to the accompanying risk, before sending it to be tokenized. Although network tokenization is not supported by all issuers, it can be extremely valuable when available.

What are the benefits of network tokenization?

Network tokenization brings many benefits, namely increased security, reduced PCI scope, and the ability to offer customers a better user experience.

Reduces Fraud and Data Theft

Because network tokenization removes the need for sensitive cardholder data to enter the payments ecosystem, it significantly reduces the risk of payment card fraud and data theft. As a result, it can help decrease declines, chargebacks, and interchange fees. In fact, in some instances, it can even shift the liability for chargebacks from the merchant to the issuer.

Positive Financial Impact for Organizations

The financial impact of these benefits is substantial, especially for enterprise organizations with high volumes of transactions. Think about it—even a marginal decrease in interchange fees and declines can have a huge impact when applied across the board to thousands—or even millions—of monthly transactions.

Try out our Network Token Calculator:

Automatic Card Detail Updates

Additionally, because the card networks are issuing the tokens, card details can be updated automatically by the card brands when changes occur. This ensures card data is always up-to-date for all payment cards on file, both improving the user experience and increasing authorization rates by preventing declines due to card expiration, loss, or theft.

Users also can enjoy features such as the ability to view digital card art when selecting a payment type for a given transaction and to use digital wallets and mobile payments where supported.

How does network tokenization improve authorization rates?

Myriad factors come together when calculating a risk score. The scope and variety of these variables can make analyzing authorization rates especially difficult. However, one of the simplest and most effective ways to increase payment acceptance rates is to reduce the overall risk of data theft or credit card fraud. Network tokens do just that.

If a processor or gateway receives a payment in the form of a network token, it will view that transaction as much less risky than one containing raw or insecure payment card details. On average, network tokens can improve authorization rates by more than 2 percent and reduce occurrences of fraud by nearly 30 percent. Again, apply those numbers to six- and seven-figure monthly transactions, and the savings really begin to add up.

Bottom line: Better authorization rates mean more revenue and better user experiences.

As card-not-present transactions have grown in popularity and profitability, so too has the opportunity for fraud. To fight this increasing risk, businesses need to introduce proven processes and technologies that can demonstrably reduce the threat cyber criminals pose to their payments ecosystems.

If sensitive payment details are compromised, or a merchant or issuer cannot verify the legitimacy of use, a transaction is usually declined. The impact of these declines goes far beyond individual transactions. Not only do declines cost businesses money, but they also hurt the user experience. They can adversely affect a business’s ability to operate and damage consumer trust. Together, these cost businesses greatly.

To combat this, network tokens help reduce risk and improve the customer experience throughout the payments process. Further, transactions that use network tokens can potentially qualify for higher authorization rates and lower interchange fees than those using standard provider tokens.

Thanks to the digital-first ecommerce boom, consumers today expect fast, frictionless transactions. When these expectations aren’t met, or even worse, if a transaction is falsely declined due to a perceived high level of risk, it can hurt your company’s reputation as well as its revenue. Contact one of our sales executives today to learn how network tokenization can fit your use case and help you begin reaping the benefits of better security, better acceptance rates, and better customer experiences.

How to Choose

a Tokenization Solution

Make sure you’re asking the right questions by this resource.