Want more content?

By subscribing to our mailing list, you will be enrolled to receive our latest blogs, product updates, industry news, and more!

Webinar Recap: The Importance of Payment Optimization and a Multi-PSP Strategy

Want more content?

By subscribing to our mailing list, you will be enrolled to receive our latest blogs, product updates, industry news, and more!

When it comes to payments, one thing is for certain – the payments industry is constantly evolving, encompassing everything from payment best practices to new payment methods. How can merchants stay abreast of changes in the payment landscape and maximize their payment optimization? One approach is to adopt a multi-payment service provider (PSP) strategy, which can help maximize revenue, business growth, and customer payment experiences.

In a recent one-hour webinar, Jeremy Layton, CEO of Verisave, and I discussed the importance of payment optimization and how to manage a multi-PSP strategy.

Webinar key takeaways:

- Stay up to date on the current state of the payment landscape.

- Learn how to enable a multi-PSP strategy without introducing complexity.

- Learn tactics to reduce your interchange fees while you increase authorization rates.

Here are a few of the biggest takeaways from this TokenEx and Verisave discussion.

Select the right payment vendors

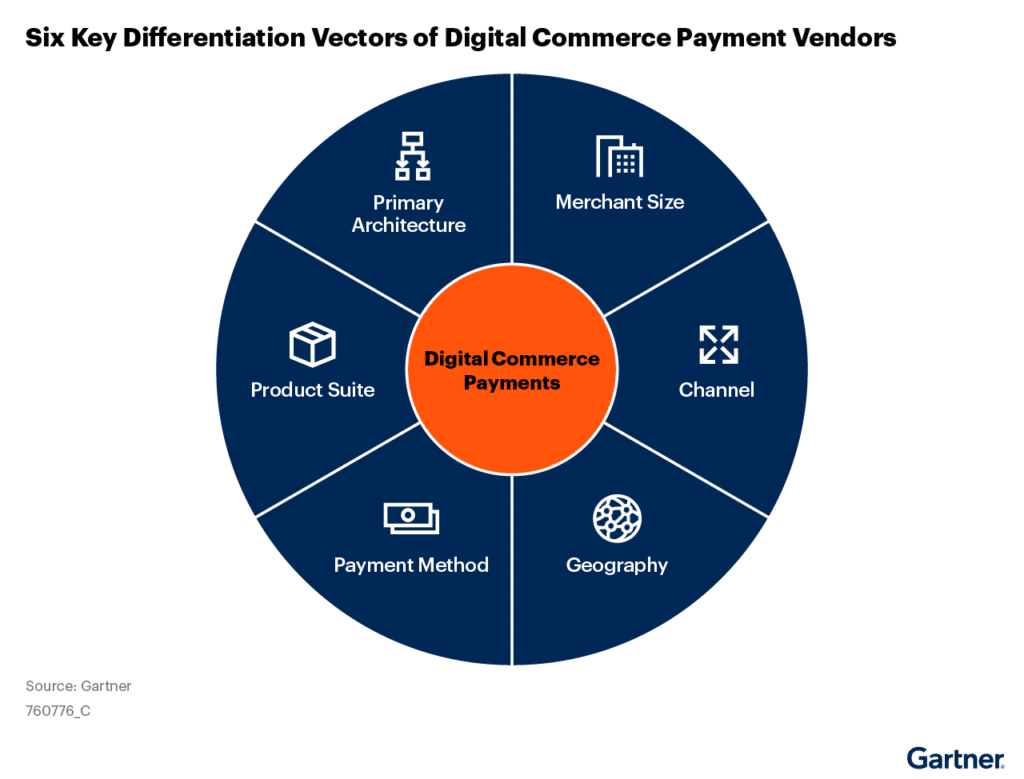

The recently published Gartner® Market Guide for Digital Commerce Payment Vendors report states, “A significant factor in a merchant’s payment vendor selection should be the existence of productized integrations from commerce, subscription, billing, or other preferred adjacent platforms.” These productized integrations can relieve the merchant from the complexities of implementing and maintaining the integrations. However, these vendor integrations may also limit a merchant’s flexibility and their choice of options when adding new features.

According to Gartner’s guide, merchants may want to consider the following six key areas of focus and differentiation for payment vendors.

Primary payment models

Gartner also notes that payment vendors typically adopt one of three models: full stack, multi-processor agnostic, or a multi-processor merchant of record or seller of record model. This is a differentiation TokenEx has observed amongst our customers as well.

With the full stack model, the vendor offers payment acceptance capabilities, back-end processing, and acquiring financial settlement. These solutions are inclusive of the customer facing payment acceptance, which feeds directly into the back-end processing capabilities.

With the multi-processor agnostic model, there is a single front-end solution for customer facing payment acceptance capabilities. This connects to the processors or acquirers of the merchant’s choosing on the back end. The merchant contracts directly with the processors or acquirers, providing the merchant with the greatest flexibility in choosing their preferred providers.

The multi-processor merchant or the seller of record model typically has one consolidated front end for consumer-facing payment acceptance capabilities supporting a multi-processor architecture on the back end. The payment vendor acts as a merchant of record and contracts directly with the processors and acquirers instead of the merchant.

Based on TokenEx’s experience with our customer base, smaller to midsize merchants tend to prefer the full-stack model, but enterprise and international merchants often require a multi-processor architecture.

Distribution of customer base

It’s also important that you select payment vendors with a customer distribution that reflects your current and anticipated future state. Most vendors will have a merchant customer distribution heavily weighted toward the smaller midsized sector or weighted toward enterprise merchants. In general, the sophistication of the vendor solution increases along with the size of their target market. For example, enterprise solutions commonly include processing redundancy, more sophisticated conversion optimization tools, stricter SLAs, and more complex pricing.

When selecting a vendor, it’s essential to consider their focus and your growth plans down the road. Will the vendor be able to support them?

Geographic coverage

The reality is that there’s not a single payment vendor that offers every digital payment acceptance method available in every country. However, there are payment vendors offering a broad, global reach. Most will remain focused on a specific region or country with limited capabilities in other locales. Ideally, you want to select a vendor or vendors that provide you with the greatest geographic coverage and potential redundancy in the geographies that you serve.

Some vendors may only be able to process transactions in specific currencies or only connect to local acquirers. For those merchants focused on a particular geographic reach, this may be sufficient. However, international companies may want to look for a global payment service provider or leverage a combination of PSPs to meet their geographic requirements.

Offer a variety of payment methods

The payment methods supported by a vendor vary with their geographic coverage. Aside from credit cards, supporting alternative and local payment methods, such as the Pix real-time payment system in Brazil or Alipay in China, can help improve a merchant’s conversion rates.

Product suite

It’s important for merchants to consider what products are most important to their business and will help them achieve payment optimization. Product suites can vary from one-stop-shop vendors to specialized solutions like fraud prevention or tokenization. Tokenization has become fairly ubiquitous among payment service providers in replacing a credit card number or other sensitive data element with a non-sensitive equivalent. However, some specialized providers give merchants more flexibility when implementing a tokenization solution. Ultimately, the best choice should be based on which services are essential for a merchant.

Adopt a multi-PSP strategy to maximize business growth

There are various reasons why merchants may choose to adopt a multi-PSP strategy. One reason is redundancy and reliability. If a merchant utilizes multiple processors and one is unavailable or is experiencing connectivity issues, the merchant can continue accepting payments by automatically routing through another processor. A second reason is the ability to negotiate for better payment processing rates and fees. For instance, merchants using a multi-PSP strategy can potentially have more leverage when negotiating those fees.

Additionally, a multi-PSP strategy provides customers with more payment options. This is crucial because certain PSPs only offer a set number of payment methods for merchants. By working with multiple processors and acquirers, merchants can provide their customers with a broader range of payment options, including credit and debit cards, digital wallets, and other ATMs.

A recent MRC study shows that, on average, merchants rely on roughly four payment processors or gateway connections and three acquiring banks to support omnichannel payments. These are averages; the number is generally higher for TokenEx’s enterprise omni-channel clients.

Single PSP limitations

Single PSPs control a merchant’s payment processes. These PSPs dictate how and where payments are routed. This can lead to missed payment opportunities via declined authorizations, which another processor could have approved.

To illustrate, by working with TokenEx, VIVRI switched to an agnostic token and now has the flexibility to use multiple PSPs, route payments to the processors with the best rates, and offer the payment options they need for their customers worldwide. These capabilities significantly increased their authorization rates by nearly fifteen percentage points and helped them gain almost seven percent in monthly revenue. This is the real power behind a multi-PSP strategy.

Multi-PSP benefits

- Achieve the flexibility to leverage multiple payment processors.

- Geographic coverage – remember, many processors only accept transactions for specific countries in specific currencies.

- Improved authorization – many merchants have a retry strategy for payment declines. If one acquirer declines a payment, the same transaction can be routed to another acquirer. This strategy is also helpful for routing transactions even when a processor is down or performing poorly.

- Access to alternative payment methods – merchants can see potentially a double-digit increase in conversion rates by adding additional payment options.

Tips to have a successful multi-PSP strategy

Tokenization

Most PSPs and acquirers offer tokenization to merchants. This type of tokenization is specific to the payment provider. Managing numerous sets of tokens for various providers can be challenging for a merchant.

Independent cloud tokenization providers enable merchants to connect with multiple processors and acquirers by providing a single universal token for a given credit card number. This capability reduces the complexity of managing various token sets or multiple tokens for a single credit card number. This is particularly important for merchants with loyalty programs or who depend on card accounts to process cardholder transactions.

Subscription models

Merchants that store cardholder data on file for subscription models or recurring payments must keep that data up to date to maximize conversation rates. Account Updater can help merchants by avoiding the friction of building cardholder data for monthly subscriptions and discovering that the card has expired or the card number has changed.

Optimize transaction routing

Whenever possible, merchants should select the least costly path for payments. A little research can pay significant dividends as your payment operations increase. Remember that merchants using a single PSP may only have one option for a specific currency or transaction type.

A BIN lookup service can assist with optimizing payments. Merchants may see different approval rates based on the BIN of a credit card. TokenEx customers select payment routes due to differing costs or authorization rates between acquirers or PSPs based on BIN ranges.

Network Tokenization

Another consideration for adopting a multi-PSP strategy is network tokenization. A network token is issued by a card network or scheme rather than an acquirer or gateway. Ideally, a merchant should select a payment vendor or independent tokenization provider that can provide the flexibility for the merchant to use their network tokens with multiple gateways or acquirers.

Payment processing fees

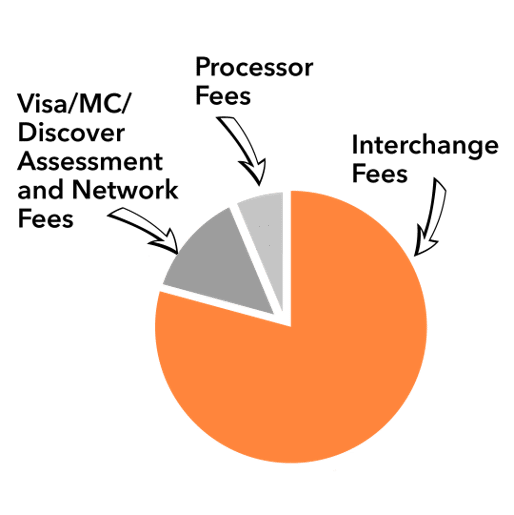

Jeremy Layton, CEO of Verisave, outlines the three main categories of fees that exist within a merchant account. These categories include interchange, assessment or network, and processor fees.

Interchange fees

Interchange fees go back to the bank that issued the card, known as the issuing bank. The bank receives most of these fees when a merchant processes a credit card payment. These fees make up about eighty-five percent of processing fees, which businesses pay when they accept card payments. Those interchange fees can fluctuate depending on the type of cards used.

Assessment or network fees

Major card networks such as Mastercard, Discover, and Visa’s assessment and network fees only make up roughly ten percent of a merchant account’s processing fees. “That’s it. Ten percent can add up to billions and billions of dollars. But again, it is the interchange fees,” Jeremy points out.

Processor fees

Payment processor fees only collect around five percent of a merchant’s total fees when they accept credit card payments. Jeremy says, “Most individuals always believe that Visa and Mastercard….are getting rich. They’re taking all of the money. In reality, it’s roughly ten percent.”

Tips to optimize your processing fees

Reduce interchange fees

If merchants want to optimize their processing fees, they should “…focus on those interchange fees,” according to Jeremy. While the impact will be minimal, this can assist merchants in reducing their overall credit card processing fees.

Jeremy notes that there are specific things merchants can do that can result in lower interchange fees. The type of card a bank issues impacts the reward that a customer receives because certain cards have higher interchange rates. Higher rates mean the bank can offer greater rewards to customers.

Proper merchant account setup

How a merchant account is set up significantly impacts the fees and charges a merchant will pay. Jeremy emphasizes, “Your merchant account may have been set up properly at the beginning, but because this industry is always changing, what once was best practices may not be [today]. You may be paying higher fees today due to your merchant account not evolving and being updated along the way.”

Adopt a multi-processor solution

Merchants aren’t the experts in processing credit card payments, and it makes sense why. The rules for processing credit cards are highly complex. Jeremy notes that Visa’s rule book has nine hundred pages of rules, along with a twenty-six-page table of contents. “That’s insane,” Jeremy says.

Due to this complexity, merchants rely on their processors to help them stay on top of these rules and evolve. This is a problem because the processors do not have the time and resources to provide individual attention to every merchant account.

Evolve with the payments industry

Jeremy suggests that merchants stay on top of the different processors’ rules, evolve with the payments industry, and be proactive about regularly asking their processors questions about improving their merchant accounts, reducing processing fees, and increasing payment optimization.